What is Phantom Tax?

Phantom Tax is a term used to describe income that needs to be taxed and other expenses that need to be accounted for, but the money has not been physically received. It commonly occurs in non-recognition transactions or where compensation is received in any form other than cash.

In other words, the type of income shown in the tax return is not covered by the real money flow, so finding the money to pay the taxes for this ‘phantom’ income becomes a problem.

Now that you understand its meaning, it’s time to know what makes it different from other kinds of taxes.

Distinctions Between Phantom Taxes And Other Kinds Of Taxes

It differs from other types of taxes in several key ways:

1. Cash Flow Impact

- Phantom: This refers to a tax on profits not transacted in cash. This tax is paid when the taxpayers do not have similar cash receipts for their management to balance the payments.

- Regular: This usually refers to cash or cash equivalent income the taxpayer receives, including wages, salaries, and business income. The tax is paid on the actual cash received basis.

2. Income Recognition Timing

- Phantom: This can occur due to differences in the timing of revenues and expenses. For instance, stock options are exercised when they turn into cash, not when they are sold.

- Regular: Usually, a tax is charged at the time of earning and receipt of income, according to the actual flow.

3. Complexity and Planning

- Phantom: Needs proper analysis and knowledge of the actual business transactions to look out for hidden tax issues. Most of the time, it requires a certain set of guidelines and computations.

- Regular: It is typically less complex as it entails planning but is more concrete regarding cash transactions and revenues.

4. Non-Cash Transactions

- Phantom: Specifically, it deals with non-cash transactions in which the transaction amount is taxable regardless of whether a cash receipt is made.

- Regular: Stresses cash and equivalent transactions, making the tax liability more predictable and conquerable.

Importance Of Phantom Tax For Businesses

Phantom taxes have many effects on business entities in all industries. They mainly concern strategic development, budgeting, and enterprise regulation.

Here’s why it is important for businesses:

1. Financial Planning and Budgeting

Phantom tax can distort an organization’s income projections by taxing income that is not actual cash income or unrealizable gains. This means businesses have to factor these scenarios into their planning to help them manage their cash flows well and prevent liquidity problems.

2. Compliance and Reporting Requirements

Companies must respect the tax rules and regulations governing phantom income. Legal consequences can occur if taxes related to phantom income are improperly reported and paid. Therefore, record keeping and knowing the current legal tax requirements are crucial to meeting these requirements.

3. Investor and Stakeholder Relations

It affects the company’s financial reporting and alters company disclosures, affecting investor perceptions and stakeholder relations. Clear disclosure of phantom income and its tax implications could improve credibility with investors by suggesting that the business is actively managing such risks.

4. Operational Efficiency

Efficient management of phantom taxes enhances operational efficiency. By including considerations of tax implications in operations and official business planning, companies can avoid wasting resources on unnecessary taxes and disruptions to normal business.

How Phantom Tax Works?

It occurs when some income is taxed, yet the taxpayer has not received cash. This results in a situation where tax is paid on ‘shadow’ income. One needs to consider the basics of income recognition to understand how it works. These circumstances lead to phantom tax, and how exactly does one compute its liability?

Mechanics of Phantom Tax

It usually arises from certain tax provisions whereby income is deemed received occasionally, even though the actual cash has not been received. Here’s how it works:

1. Income Recognition

Tax laws require specific forms of income to be accounted for when they are earned or vested, not when they are received in cash. This can encompass noncash benefits, receivables, or deferred revenues.

2. Tax Liability Creation

When recognized, this income is included in the taxpayer’s gross income for the particular year. This raises the taxable income and generates a tax amount that must be paid in taxes.

3. Payment Without Cash

The taxpayer has to look for the cash to pay taxes on this recognized income, though no cash has been received. This often puts pressure and strain on cash flow and entails financial management.

Examples Of Phantom Tax Scenarios

Here are some prime examples of its scenarios:

Unrealized Gains on Stocks

Unrealized gains include situations where a taxpayer still possesses an asset that has appreciated but has not sold it. For instance, if an investor has shares of appreciated stock, the increase in value remains an unrealized gain until the shares are disposed of.

Implication

- No legal tax provisions normally require individuals and companies to pay taxes based on unrealized gains. Nevertheless, in some circumstances, such as when the shares are passed to another party or individual, such gains may be subject to tax.

- Although investors might not have received the money in cash, they might be called upon to report the increase in value as taxable income.

Depreciation in Real Estate

Depreciation in real estate enables the property proprietors to write off an amount representing the cost of the property over the expected years of usage. While it lowers taxable income, this non-cash expense does not represent the actual cash outflow.

Implication

- Once a property is sold, all the depreciation taken over the years must be added back to the taxpayer’s taxable income and is taxed at the ordinary rate. This may increase tax payable even though depreciation allowances were non-cash expenses.

- Some property owners will end up paying hefty tax amounts for recaptured depreciation. Hence, they need to plan how to meet such taxes, especially when they are due.

Zero-Coupon Bonds

Zero-coupon bonds are issued substantially lower than their face value and do not receive interest payments. However, interest is compounded and paid at the time of redemption for its face value on the due date.

Implication

- The bondholders report some of the imputed interest annually as taxable income to the IRS, even though no cash payments are made throughout the contract period until the debt matures.

- Thus, investors are liable to pay taxes on this imputed interest yearly despite no cash flow from the bond until it is redeemed.

Implications Of Phantom Tax

Here are some key implications financial managers must consider:

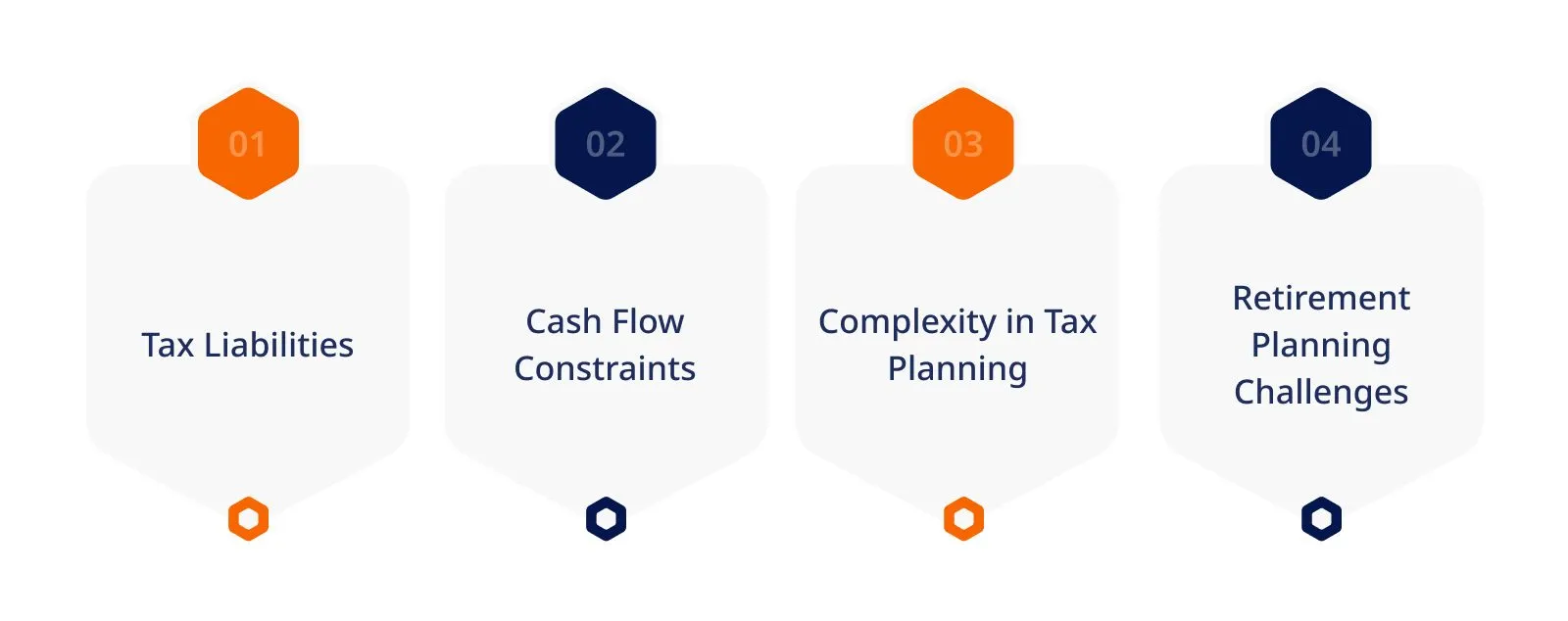

1. Tax Liabilities

Like lock-in taxes, phantom taxes involve taxing income not transacted in cash. People must recognize and pay taxes on fictional income, thus raising their taxable income and the taxes they pay despite having no cash. Planning for such taxes and ensuring adequate funding to cater for these expenditures is crucial.

2. Cash Flow Constraints

It results from the accrual accounting method, which deals with non-cash income and thus impacts cash flow. This often requires individuals to liquidate their assets, use personal savings or reverse roles, and borrow money to pay taxes, thus exerting pressure on cash flows.

3. Complexity in Tax Planning

This similarly affects tax planning due to complex tax recognition arrangements. Taxpayers must always look for possible situations that might lead to phantom income and include them in their taxation strategies, which can be challenging without professional advice.

4. Retirement Planning Challenges

It refers to taxes that arise from specific retirement plans and structures, resulting in changed tax systems and plan structures. They are also likely to experience tax shocks on recognized income that has not yet been received and, therefore, need strong and adaptable retirement plans to absorb these costs.

Manage Phantom Tax With Invoicera

Invoicera can help financial managers manage this tax effectively by providing tools and features that streamline financial planning and reporting:

- Automated Invoicing: The main feature is invoicing, where the software helps generate invoicing data realistically and on time, recording and accounting for every income, including phantom income.

- Expense Management: It might be easy to record and classify deductions to eliminate phantom income by claiming legitimate business expenses to lower overall taxes.

- Cash Flow Management: With timely financial information, businesses can hold sufficient cash to meet phantom tax amounts without experiencing cash flow problems.

- Detailed Financial Reports: Prepare detailed financial statements to look for phantom income and determine likely future taxes.

- Tax Compliance Tools: Using Invoicera’s tax management tools is recommended to avoid tax violations and subsequent fines with interest for unpaid taxes.

- Consultation and Support: Seek professional assistance on tax planning and dealing with complicated financial issues, particularly phantom tax.

In this way, phantom tax can be easily planned and managed to achieve the best results using the finance management tools available on Invoicera.

Steps To Minimize Phantom Tax For Businesses

Here are steps financial managers can follow to minimize this tax for businesses:

1. Identify Potential Phantom Income Sources

The first step is to comprehensively list all probable phantom income sources in the company. This includes stock options, equity, partner income, deferred wages, and canceled debts. It is helpful in planning and avoiding its effects to know where phantom income might occur.

2. Implement Strategic Income Recognition

When recording income, ensure it coincides with the actual flow of cash. For instance, when dealing with stock options, businesses can plan for the vesting period to occur during a period of high liquidity. Likewise, controlling the timing of unused compensation payments can assist in matching taxation with revenues.

3. Optimize Compensation Structures

Conduct a review of compensation structures to avoid instances of phantom income. For example, opt for fixed cash instead of stock options or adopt non-tax qualified deferred compensation schemes with flexibility over income recognition and payment.

4. Use Tax-Advantaged Accounts

Use tax shelter accounts and conduits to minimize phantom income. For instance, contributions to retirement savings or HSAs can decrease taxable income and counterbalance phantom income tax liability.

5. Maintain Adequate Reserves

Ensure you have enough cash in your business to meet any phantom tax that might be owed. Maintaining a sufficient level of cash on hand enables the business to make payments to the relevant tax authorities without liquidating valuable assets at unfavorable prices.

6. Consult with Tax Professionals

Consult with tax professionals to develop and execute solutions applicable to the unique business. Professional tax advisors can help individuals deal with phantom income problems, explain taxation rules, and help with overall tax planning.

7. Stay Informed on Tax Laws and Regulations

Be aware of changes in common tax provisions that have implications for phantom income. Updating the business’s tax strategies enables the company to comply with legal requirements to which it is subject, and it ensures that it does not miss out on opportunities to reduce taxes whenever there is a change in legislation.

8. Monitor and Review Financial Statements

Maintaining and reviewing financial statements regularly to prevent and eradicate phantom income at its root. Continuous financial monitoring is useful for making appropriate modifications and managing taxes.

Closing Thoughts

In conclusion, Phantom tax refers to a situation where income is reported on the tax return, although it was not received in cash during the same or a previous period. It is often used in cases such as share options and retirement benefits among employees, but it needs to be well administered.

Some solutions that can reduce its effects include income smoothing, maintaining sufficient reserves, and seeking advice from tax advisors. Therefore, financial managers should assess and prevent these issues to maintain an adequate financial status regarding taxes.

Hopefully, this blog successfully explained the meaning of the phantom tax and covered other important aspects of the concept.

FAQs

Q: What are the consequences of not addressing phantom tax liabilities promptly?

Ans: Neglecting its liabilities may result in penalties, interest accrual on unpaid taxes, and monetary pressure due to unforeseen tax demands. These liabilities must also be controlled and properly planned for.

Q: Are there specific tax strategies to help mitigate phantom tax for high-income earners?

Ans: Yes, certain strategies that may effectively deal with it include tax-sheltered investment plans, charitable contributions, and creative compensation strategies. It is always wise to consult your financial adviser or an accountant for a properly tailored strategy.

Q: How do changes in tax laws impact phantom tax liabilities?

Ans: Phantom taxation can change due to adjustments in the tax legislation involving the timing or amount of taxation. People and companies must get updates on any tax changes and seek advice from tax advisors to avoid incurring high taxes.