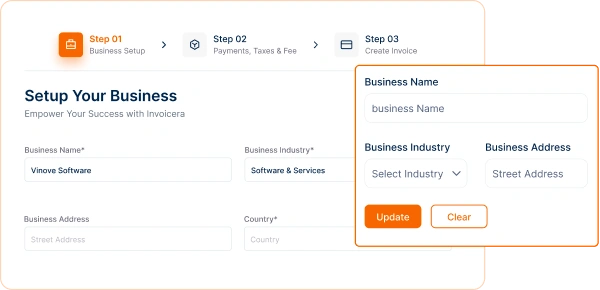

Discover the Magic of Automated Invoicing

Slash costs by 70%. Begin your automated invoicing journey in minutes.

Safeguard your business from fraudulent activities, ensuring secure and reliable payment processing.

Invoicera’s secure invoicing features help you prevent invoice fraud and maintain the integrity of your payment system.

Invoicera provides customizable, tamper-proof invoice templates, making it nearly impossible for anyone to alter or forge your invoices.

Automated e-invoice verification system cross-checks invoice details against your existing data, reducing the risk of fraudulent activities.

Invoicera implements advanced security measures to safeguard your data from unauthorized access and potential breaches.

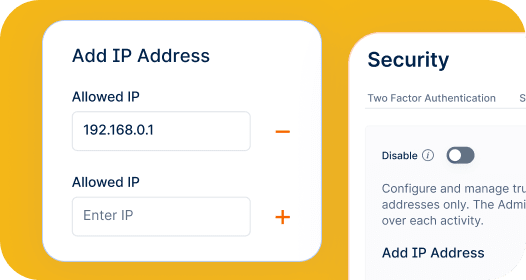

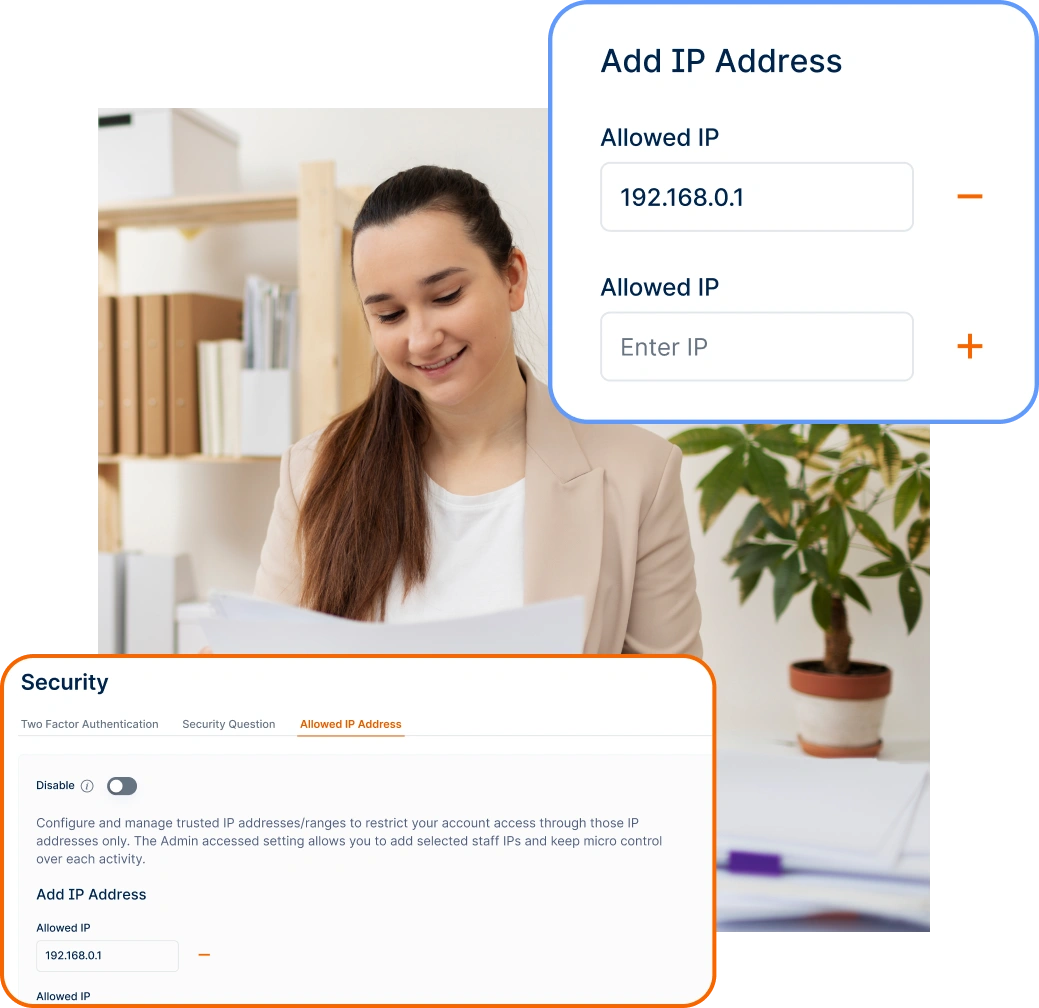

Strong password policies prevent unauthorized access to your account.

All data transmission between your browser and Invoicera servers is encrypted using industry-standard protocols.

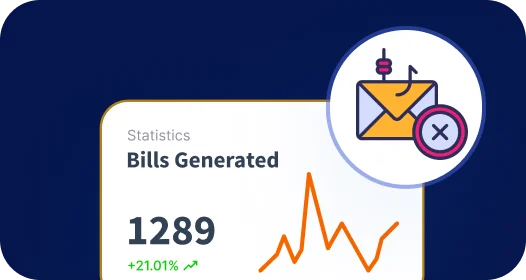

Get real-time insights for efficient financial management and seamless business progress.

A SaaS company reduced manual work by 60% using Invoicera’s automated recurring billing, invoice scheduling, and reminders.

Get Started with Smarter Billing

Digital marketing firm increased payment collection with Invoicera’s automated invoicing, project hour tracking & follow-up reminders.

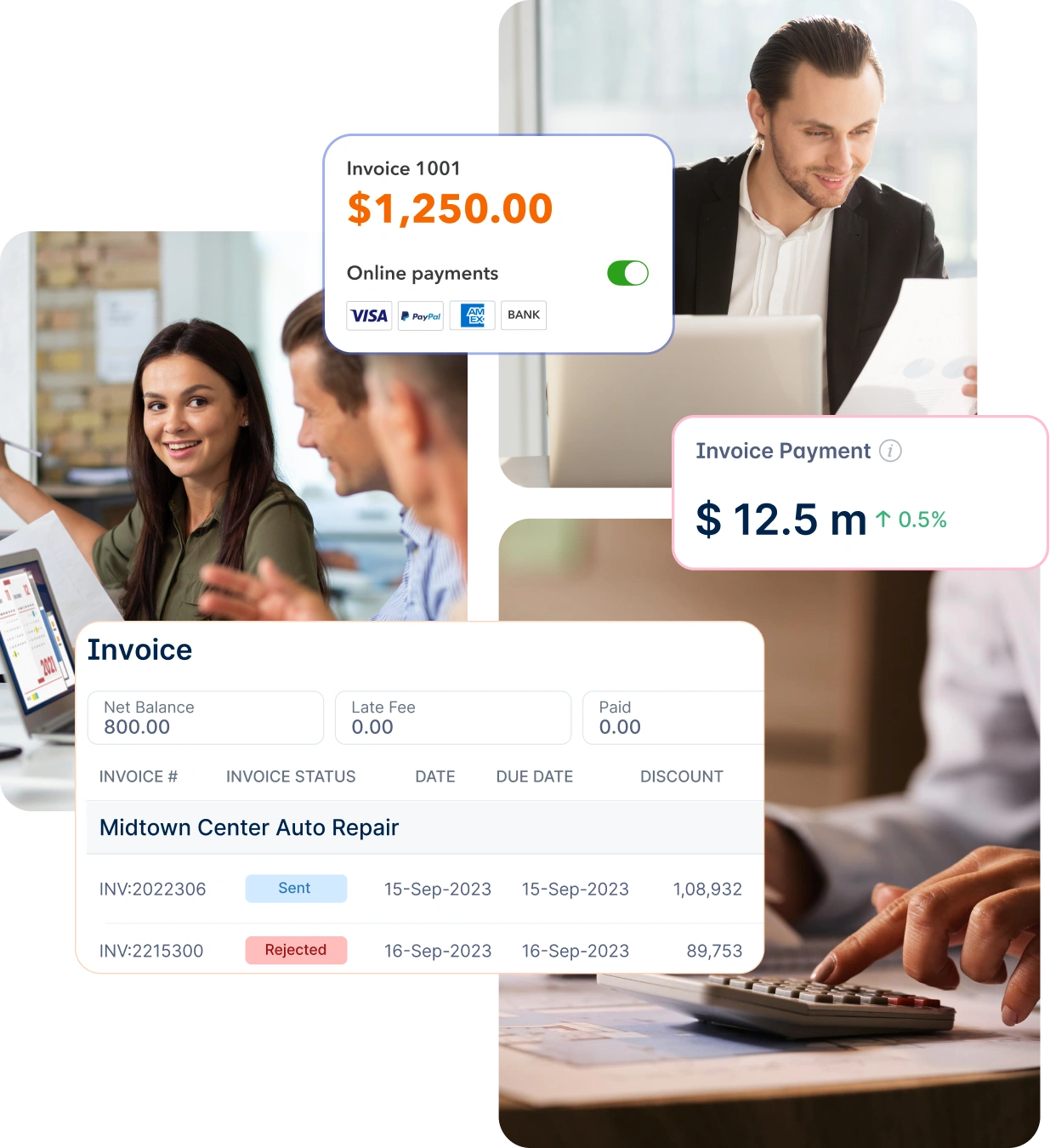

Improve Your Cash FlowInvoicera integrates with trusted and secure online payment methods, giving you peace of mind regarding your online transactions.

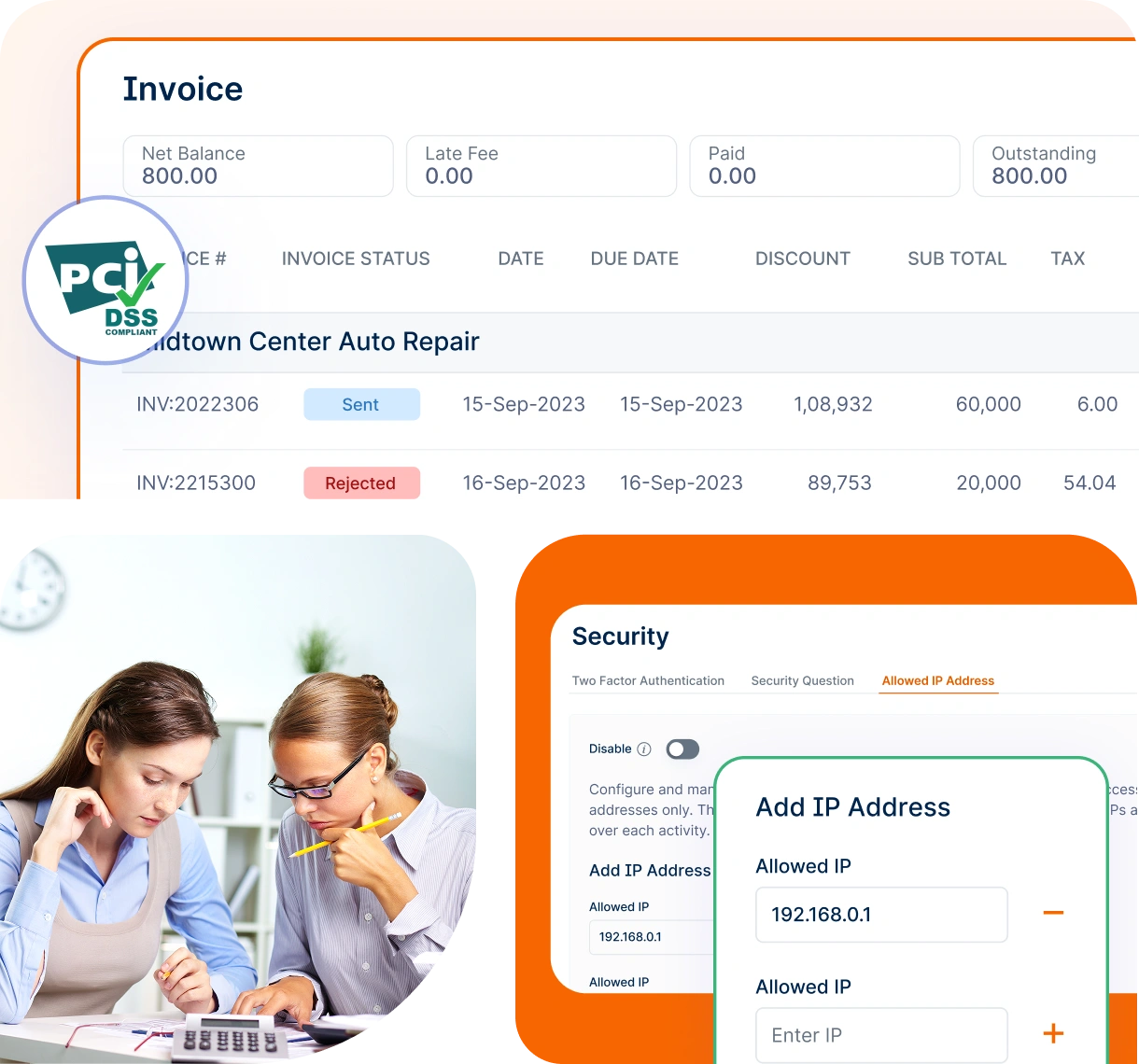

Invoicera complies with the Payment Card Industry Data Security Standard (PCI DSS), ensuring the security of your payment data.

Your payment information is tokenized and encrypted before being stored, protecting you from data breaches.

Ready for the most-secured billing process? Here’s how to start your invoicing journey with Invoicera.

Log in to your Invoicera account to access secure invoicing features.

Activate 2FA from the Apps & Integrations settings for added security.

Send and manage invoices securely, protecting your data from fraud.

All-in-one invoicing software to manage & track payments, expenses, bills & more.

Maximize your revenue and drive growth with efficient invoicing.

Create professional invoices in minutes. Automatically add tracked time and expenses.

Learn MoreOptimize your finances with credit control, secure payments & streamlined cash flow.

Learn MoreManage everything in one place - time, estimates, and more, hassle-free.

Learn MoreStay safe and in control with our watchful eye on your data and smooth admin tools.

Learn MoreScale effortlessly with a platform that adapts to the unique needs of any business, large or small.

Stay on top of your cash flow

Turn hours into accurate invoices

Master complex billing effortlessly

Discover reliable payment integration gateways, offering diverse

payment options tailored to your business needs.

No, fraud protection is important for businesses of all sizes. Small businesses can be particularly vulnerable to invoice fraud, making it crucial for them to have adequate protection in place.

If you suspect any fraudulent activity on Invoicera or have security concerns, please contact our support team immediately. We take such matters seriously and will investigate promptly.

Invoicera helps prevent fraud by offering secure invoicing, encrypted transactions, role-based access controls, and real-time monitoring of financial activities. With automated invoice validation, fraud detection algorithms, and compliance with global security standards, Invoicera ensures safe and transparent transactions.

The basic fraud protection features are included in your Invoicera subscription. You might contact our support team to know if there is any additional cost for highly advanced security features.

Invoicera implements multiple security measures, including:

✅ End-to-End Encryption – Protects sensitive payment data.

✅ AI-Powered Fraud Detection – Identifies unusual transaction patterns.

✅ Role-Based Access Control (RBAC) – Restricts user permissions to prevent unauthorized actions.

✅ Invoice Verification – Flags duplicate or altered invoices.

✅ Audit Logs & Reporting – Tracks user activity for enhanced oversight.

Yes, Invoicera offers real-time fraud detection by continuously monitoring transactions and flagging unusual activities. The system analyzes payment behavior, detects anomalies, and alerts businesses about potential risks, helping them take immediate action.

Yes, Invoicera can detect and block suspicious transactions through automated risk analysis. It identifies unusual payment behavior, flags potentially fraudulent invoices, and restricts high-risk transactions based on predefined security rules. Businesses can set up alerts and automate approval workflows to prevent unauthorized payments.

Yes, Invoicera supports multi-factor authentication (MFA) to enhance payment security. This ensures that only authorized users can process payments by requiring multiple verification steps, such as passwords, OTPs, or biometric authentication, reducing the risk of unauthorized access and fraud.

We value your feedback and love sharing user experiences.

For my contractor business, I needed a solution that replaces an outdated manual invoicing system. Invoicera made it simpler and easier to invoice. Now, I spend less time manually and more time to help clients with their queries. Incredibly intuitive invoicing software.

When I began my real estate firm, I hated invoicing so much that sometimes I put off sending invoices for months. Invoicera proved to be the best online invoicing platform that caters to professionalism and quickly sent out estimates and invoices on the spot.

No complicated software, easy-to-use interface with definite benefits from fast invoicing, expense tracking, estimates, billing, advanced sales tax and more. Great app for both beginners and advanced users. Now I can look for the detailed financial performance overview and efficiency of people working on billed, unbilled and internal projects. You can easily analyze profit, loss and cash flow.

When running the hotel business, controlling business expenses and maintaining surplus cash flow became hectic for me. I wanted a solution that could take my hospitality business to the next level. With rapid research on the internet, I found Invoicera that control all my hotel business expenses with ease. Thank You. Great program.

Streamline billing and generating invoices with Invoicera.

Invoicera is a true value for money software. It offers great features which are suited to all professions.

Explore MoreThe best Invoice app for managing your finance and generating online invoices. Simple to create invoices and to share with our customers.

Explore MoreStart Risk-Free. No Credit Card Needed. Cancel Anytime.

Seamless integration with your existing software.

Fortify account security with 2-factor authentication, IP address restriction & automated data backups.